iDollar: Are Stablecoins Apple’s Next Multi-Billion Dollar Play?

With the GENIUS Act signed into law, could a company like Apple launch its own stablecoin? We break down what the iDollar could look like here.

For years, Apple has been slowly but surely stepping into the banking world. But now, with the GENIUS Act signed into law and providing a pathway for any company to issue its own stablecoin, Apple may be ready to make its biggest financial move yet.

The prize? Over $30 billion in incremental, high-margin profit and even greater control over the global financial stack.

Here’s our breakdown of what an iDollar could do for Apple.

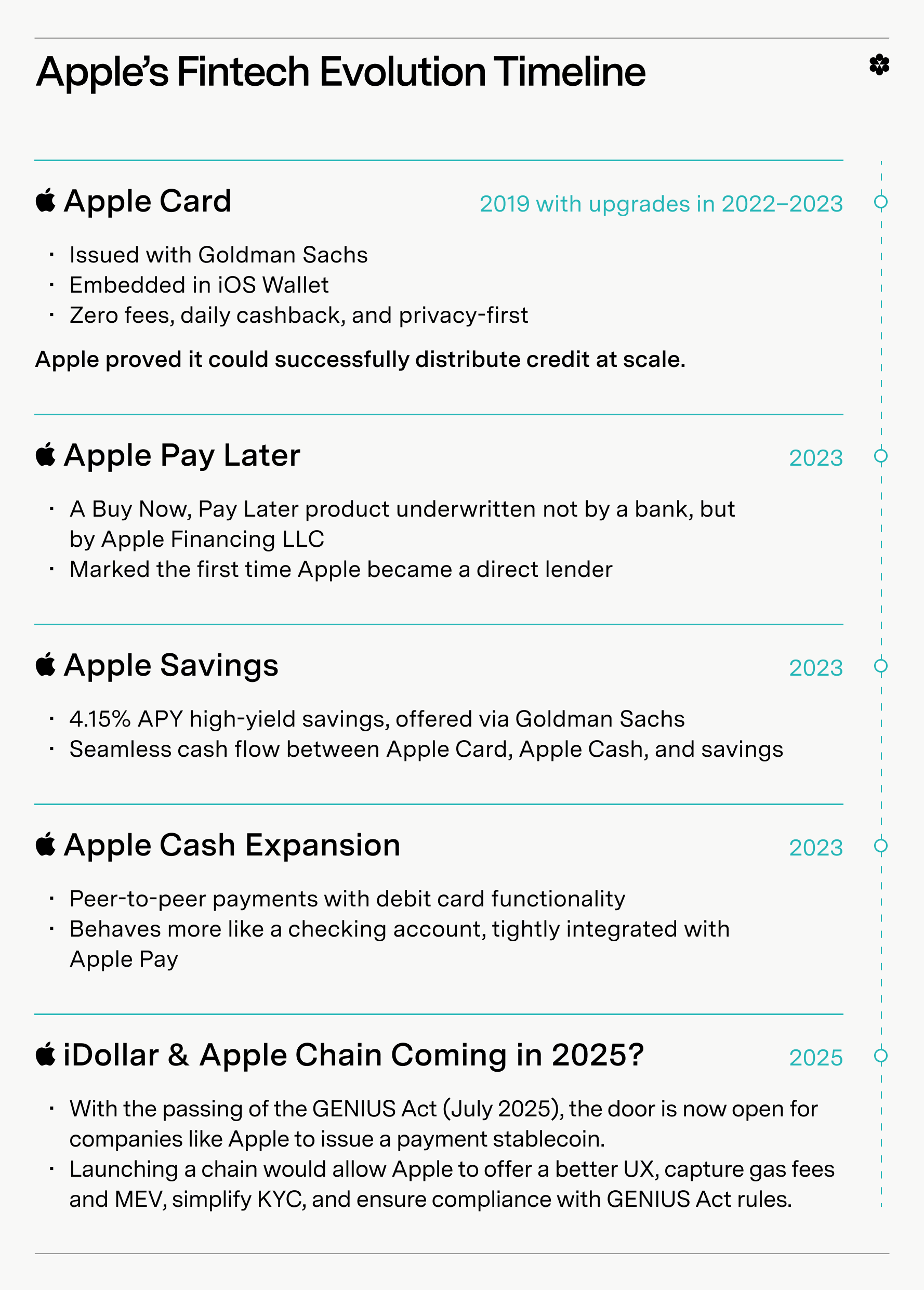

Apple’s banking playbook (so far)

Together, these moves positioned Apple as more than a fintech partner but as a quasi-bank with one of the world’s most powerful financial UX stacks.

Why people say “Apple will be a bank”

Each of Apple’s financial product launches reinforced the same narrative: Apple is a tech-native financial services company, not just a hardware company.

- Financial infrastructure ownership: Apple now handles underwriting, lending, KYC, and UX directly.

- Massive distribution moat: 1B+ iPhones ready to activate financial products in one tap + an estimated 65.6 million Apple Pay users in the US alone.

- Brand trust + liquidity: Apple has the capital and user trust traditional banks envy.

- Full-spectrum services: Credit, payments, savings, and peer-to-peer flows all under one roof.

But there was still one missing piece.

Enter: iDollar

With the passing of the GENIUS Act (July 2025), the door is now open for companies like Apple to issue a payment stablecoin fully backed by T-bills and other high-quality liquid assets without registering as a bank or securities issuer.

And the upside? Monumental.

A GENIUS-compliant “iDollar” could:

- Replace FDIC pass-through funds with T-bill-backed coins

- Earn 4.3% yield on idle wallet balances

- Slash card-network fees

- Enable real-time cross-border payments

- Expand programmable payments across Apple’s ecosystem

- Future-proof Apple Pay against interchange regulation

- Deepen customer loyalty with iDollar discounts and incentives (“10% off your next iPhone upgrade if you pay in iDollars!”)

- Offer opportunities to access DeFi yield or buy tokenized stocks from players like Robinhood, directly from the Apple Wallet

In short, Apple could flip a zero-yield liability into a multi-billion-dollar flywheel.

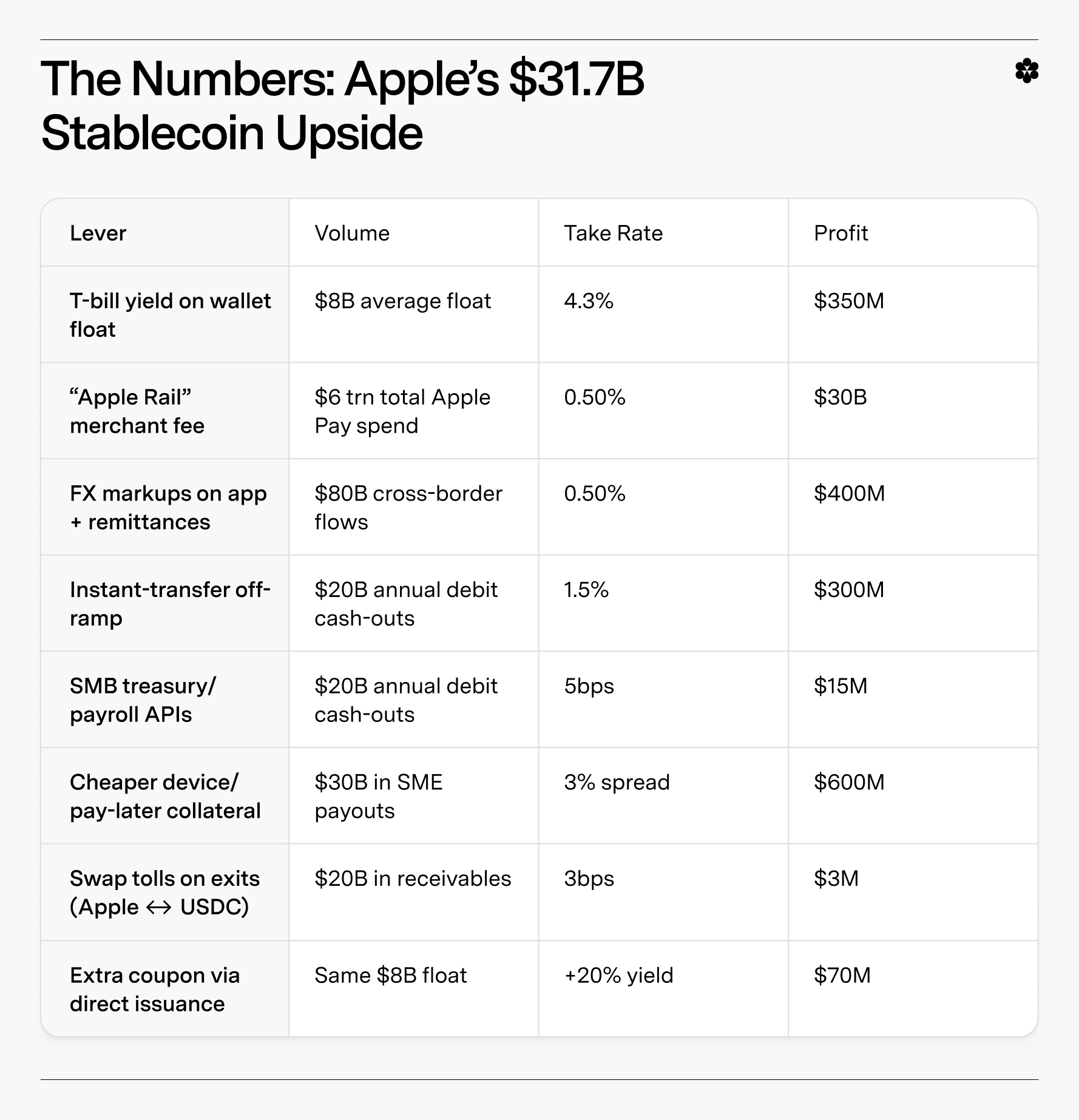

The numbers: Apple’s $31.7B stablecoin upside

Here’s what that upside looks like in practice:

Total: $31.7 billion/year in new profit without overhauling the UX or requiring a hardware update.

How Apple could launch it

Option A: White-label via Agora

- Launch instantly with an Apple-branded coin issued by Agora (a licensed PPSI under the GENIUS Act)

- Apple earns a cut of the yield + controls the UX and brand

Option B: Build in-house

- Apply for a GENIUS PPSI charter

- Take full control of the issuance, reserves, and economics

- More effort, but 100% yield capture

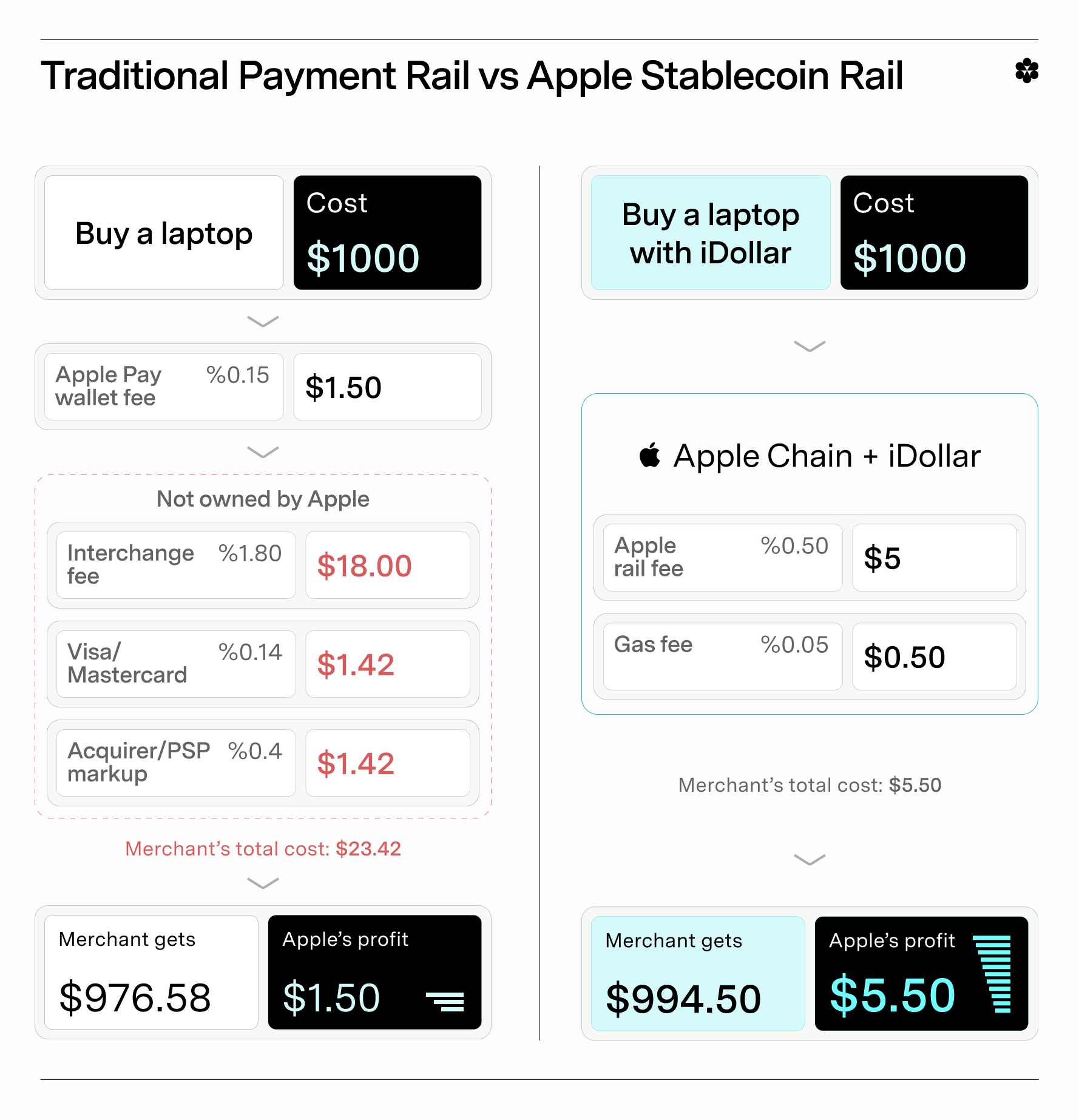

Issue on Apple Chain

The next question for Apple would be where to issue the iDollar. While the token could be bridgeable to many chains, launching a dedicated chain to act as its primary home for minting and usage would benefit Apple in several ways.

- Value capture: A dedicated chain would allow Apple to capture all gas fees and MEV directly, and leak as little value as possible to third parties.

- Better UX: If there’s one thing Apple cares about, it’s UX. A dedicated chain would enable Apple to lower latency for instant transfers, avoid network slowdowns, and set iDollar as the gas token for convenience.

- Compliance: A dedicated chain would make it easier for Apple to KYC users, create whitelists for who can deploy contracts that touch iDollar, and comply with GENIUS Act rules around token freezes and clawbacks.

A dedicated chain for iDollar would improve the product’s economics and fit with Apple’s ethos of owning and optimizing all elements of the user experience.

Apple’s strategic edge goes beyond profit

Launching a stablecoin doesn’t just unlock revenue. It also gives Apple powerful strategic leverage:

- End-to-end control of payments UX (no Visa/Mastercard approval needed) today Over 90% of U.S. retailers accept Apple Pay.

- 24/7 global settlement (cross-border, in-app, royalties, B2B)

- Programmable developer rails (wallets, escrow, micropayments)

- Customer loyalty and greater share-of-wallet with iDollar discounts and incentives

- First-party data visibility (better fraud and credit models)

- Onchain compliance controls (freeze, whitelist, geo-fence)

- Optional interoperability (swap bridges keep users in ecosystem)

- Regulatory hedge (protection against interchange caps or payment mandates)

- Narrative fit (“Secure. Private. Apple-backed money.”)

The final piece of Apple’s financial stack

Apple doesn’t need to become a bank. It just needs to control the rails.

With the GENIUS Act now live, Apple has the legal framework, technical infrastructure, and economic incentive to flip its financial stack into a yield-generating, real-time payment engine.

No new hardware. No massive regulatory risk. Just a software update and a stablecoin.

The “iDollar” era may have just begun.

Interested in learning more about how blockchain technology could improve your business? Book a quick demo to learn how.